Touching Distance

Following a flurry of consistent new ATHs, Bitcoin is just a stone's throw away from reaching a price of $100k per coin. Explosive price action tends to result in a significant increase in the unrealized profit of holders, and Long-Term Holders are ramping up their distribution in response.

Executive Summary:

- As the Bitcoin price rallied towards $100k, Long-Term Holders commenced distributing over 507k BTC, which remains less than the 934k BTC sell-side during the March rally but is significant nonetheless.

- Long-term holders are locking in sizeable profit volumes, setting a new ATH of $2.02B in daily realized profit.

- When assessing the composition of which entities are spending, the majority of this sell-side pressure appears to originate from coins aged between 6 months and 1 year.

Intense Long-Term Holder Distribution

Following a flurry of consistent new ATHs, the Bitcoin price is now within striking distance of the impressive and long-awaited value of $100k per coin. Like all previous cycles, the Long-Term Holder cohort is taking advantage of inflowing liquidity and a strengthened demand side to recommence distribution of held supply at scale.

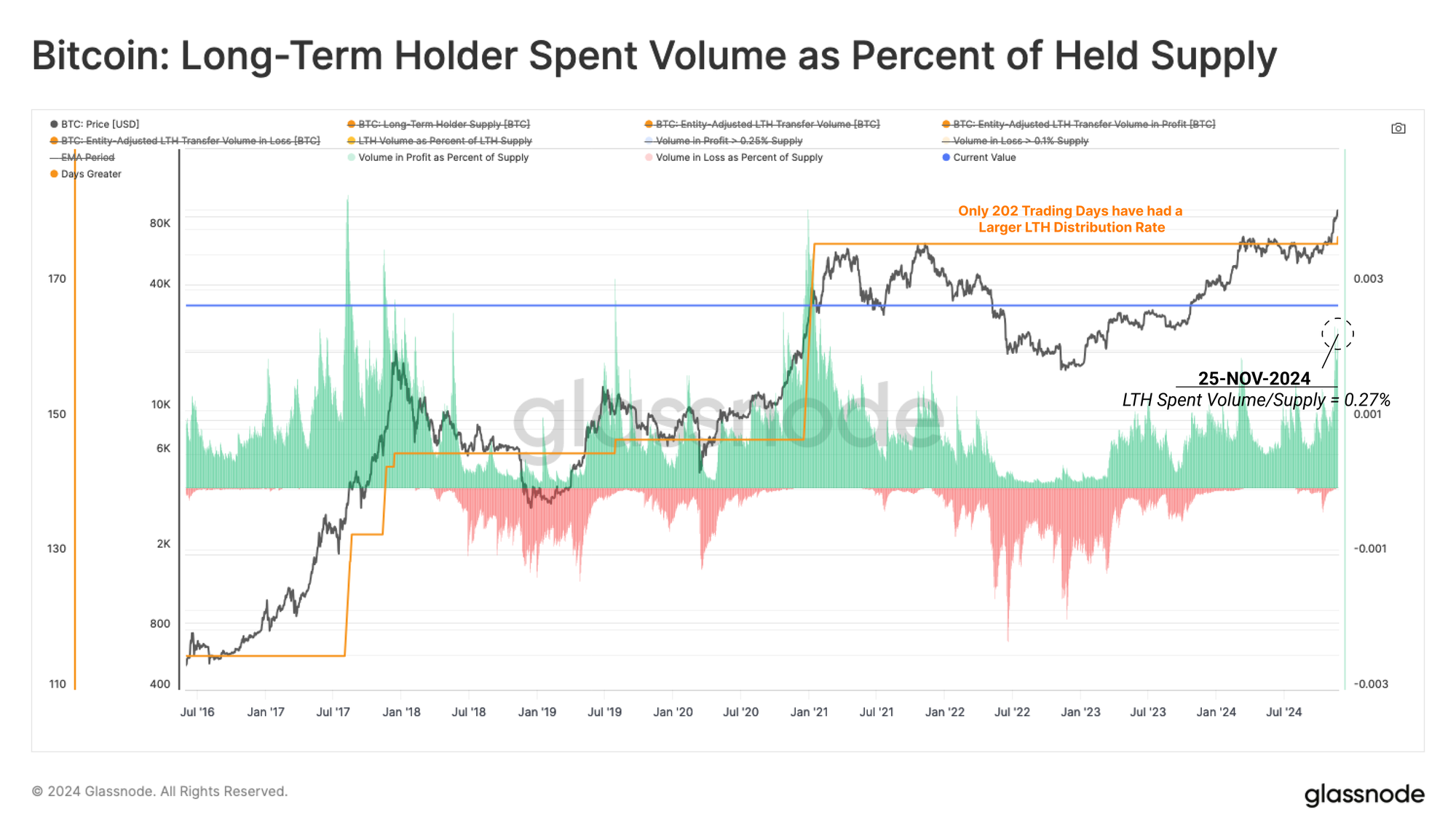

Since the peak in LTH supply set in September, this cohort has now distributed a non-trivial 507k BTC. This is a sizeable volume; however, it is smaller in scale relative to the 934k BTC spent during the rally into the March 2024 ATH.

We see a similar story by assessing the percentage of aggregate Long-Term Holder supply transacted from a profitable position. Currently, an average of 0.27% of the LTH supply is being distributed daily, with only 177 out of all trading days recording a heavier distribution rate.

Interestingly, we can observe that this relative rate of LTH spending is larger than the March 2024 ATH, underscoring a more aggressive distribution campaign.

We can also consult the LTH Liveliness metric to evaluate the balance between Coinday creation (holding time) and Coinday Destruction (spent holding time). Typically, Liveliness uptrends are characterized by an environment of heightened spending activity, whereas downtrends denote that HODLing is the primary dynamic.

While the current rate of supply distribution is greater than the March peak, the volume of Coinday destruction remains lower. This highlights that most LTH coins transacting are likely to have been acquired relatively recently (e.g., more likely to be 6 months old than 5 years old on average).

Profits Locked In

Long-Term Holders have a key role in the price discovery process, as they are a dominant source of previously dormant supply returning into liquid circulation. It becomes more prudent to assess the degree of profit-taking amongst this cohort as the bull market progresses, as they tend to become increasingly more active as prices rise.

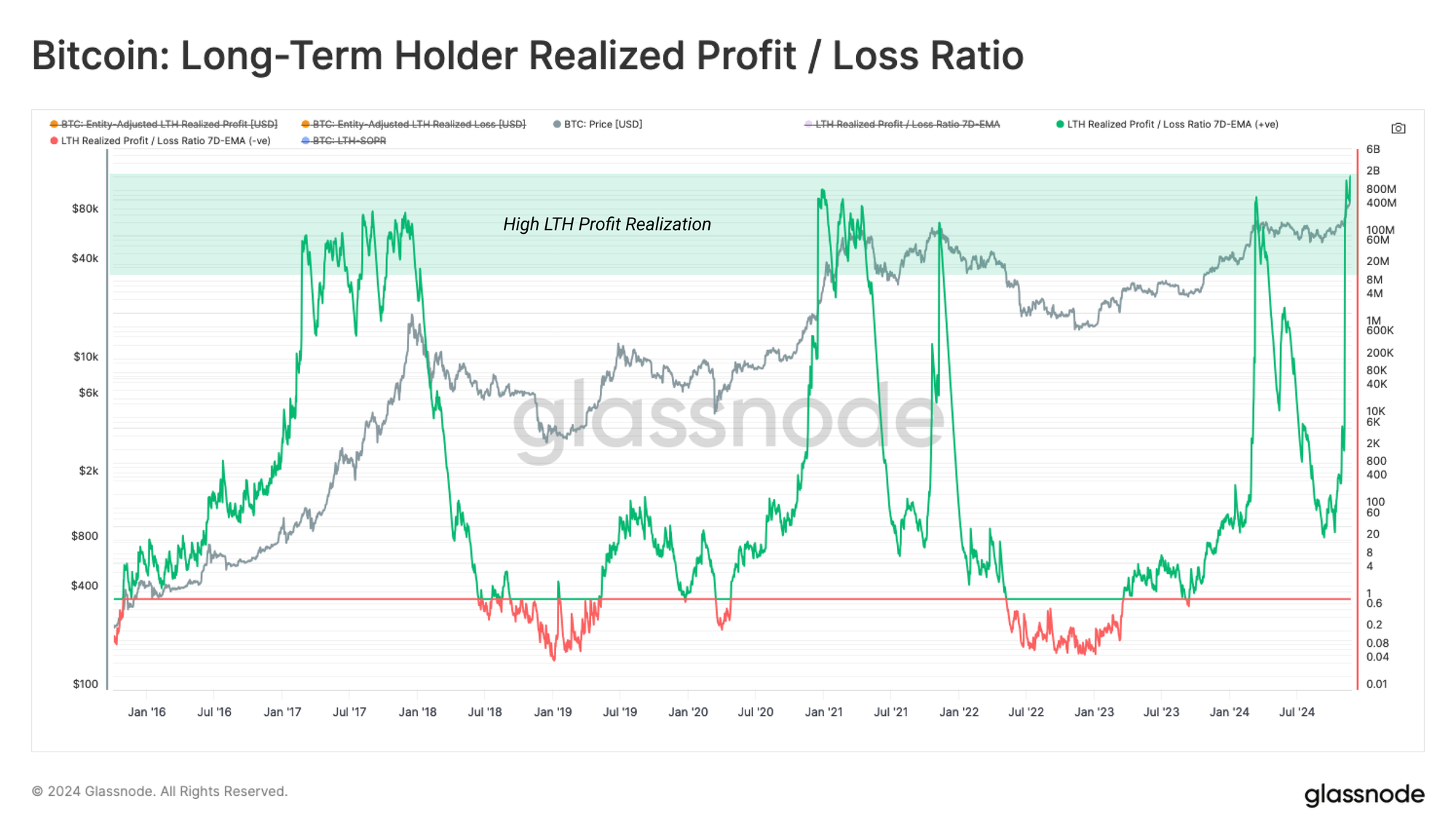

Long-Term Holders are currently realizing a massive $2.02B in realized profit per day, setting a new ATH and eclipsing the previous one set in March. A robust demand side is required to fully absorb this supply overhang, which may require a period of re-accumulation to fully digest.

Assessing the balance between profit and loss volumes taken by LTHs, we can see that the ratio of the two has accelerated rapidly in November. By definition, this results from the lack of LTH supply held in loss during this price discovery regime.

Historically speaking, the price has remained within a euphoric state for several months, assuming there is a substantial and consistent inflow of fresh demand.

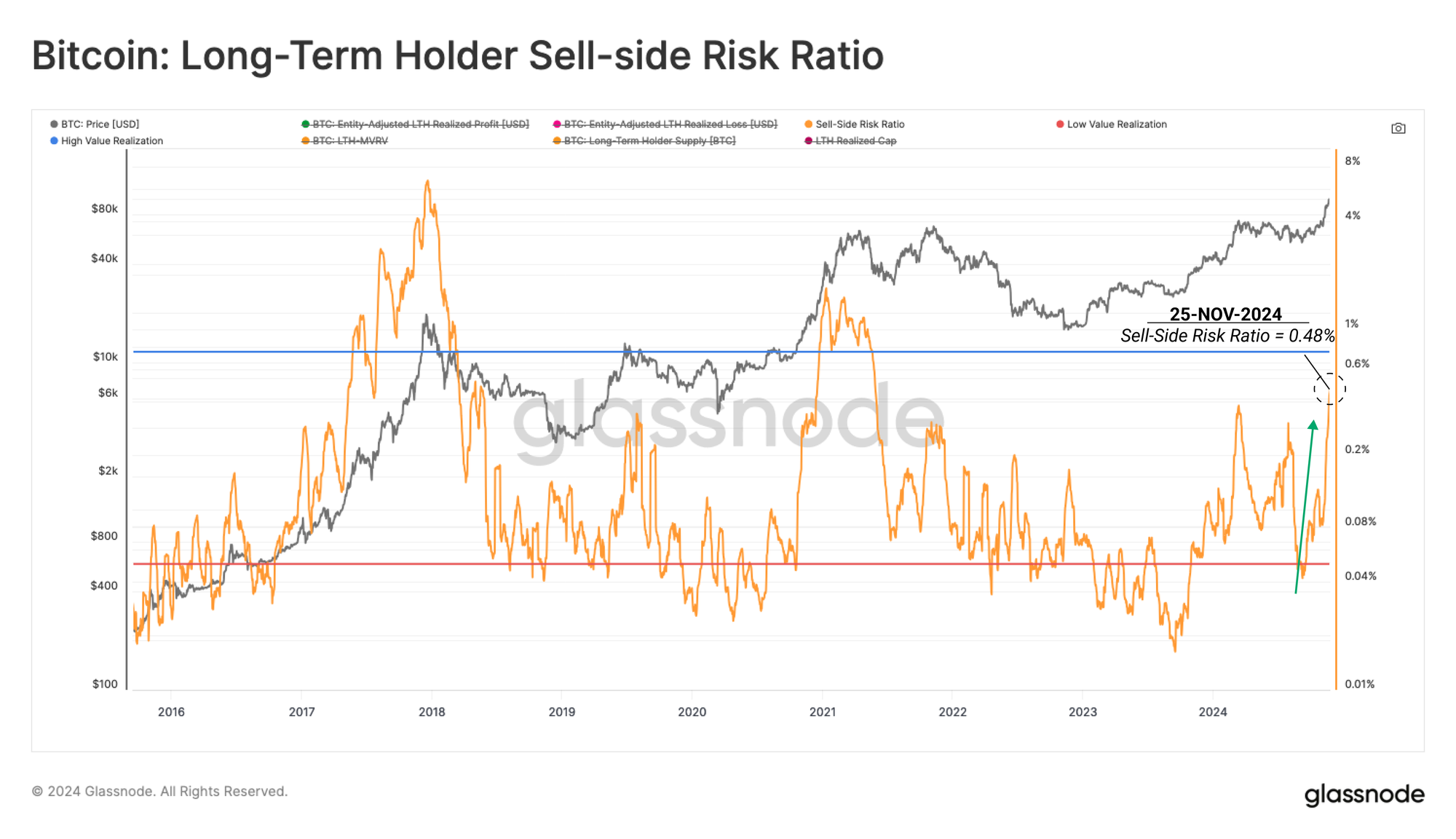

The Sell-Side Risk Ratio assesses the total volume of both realized profit and loss locked in by investors relative to the asset size (measured via the Realized Cap). We can consider this metric under the following framework:

- High values indicate that investors spend coins at a significant profit or loss relative to their cost basis. This condition indicates that the market likely needs to re-find equilibrium and usually follows a high volatility price move.

- Low values indicate that most coins are being spent relatively close to their break-even cost basis, suggesting a degree of equilibrium has been reached. This condition often signifies an exhaustion of ‘profit and loss’ within the current price range and usually describes a low volatility environment.

The Sell-Side Risk ratio is approaching the high-value band, inferring that significant profit-taking is occurring within the current range. Nevertheless, the current reading remains substantially lower than the terminal value reached in prior cycles. This suggests that previous bull markets have seen sufficient demand to absorb supply, even under similar relative distribution pressures.

The Composition of Spending

Having established a significant uptick in Long-Term Holder profit-taking, we can increase the granularity of this assessment by scrutinizing the composition of the supply sold.

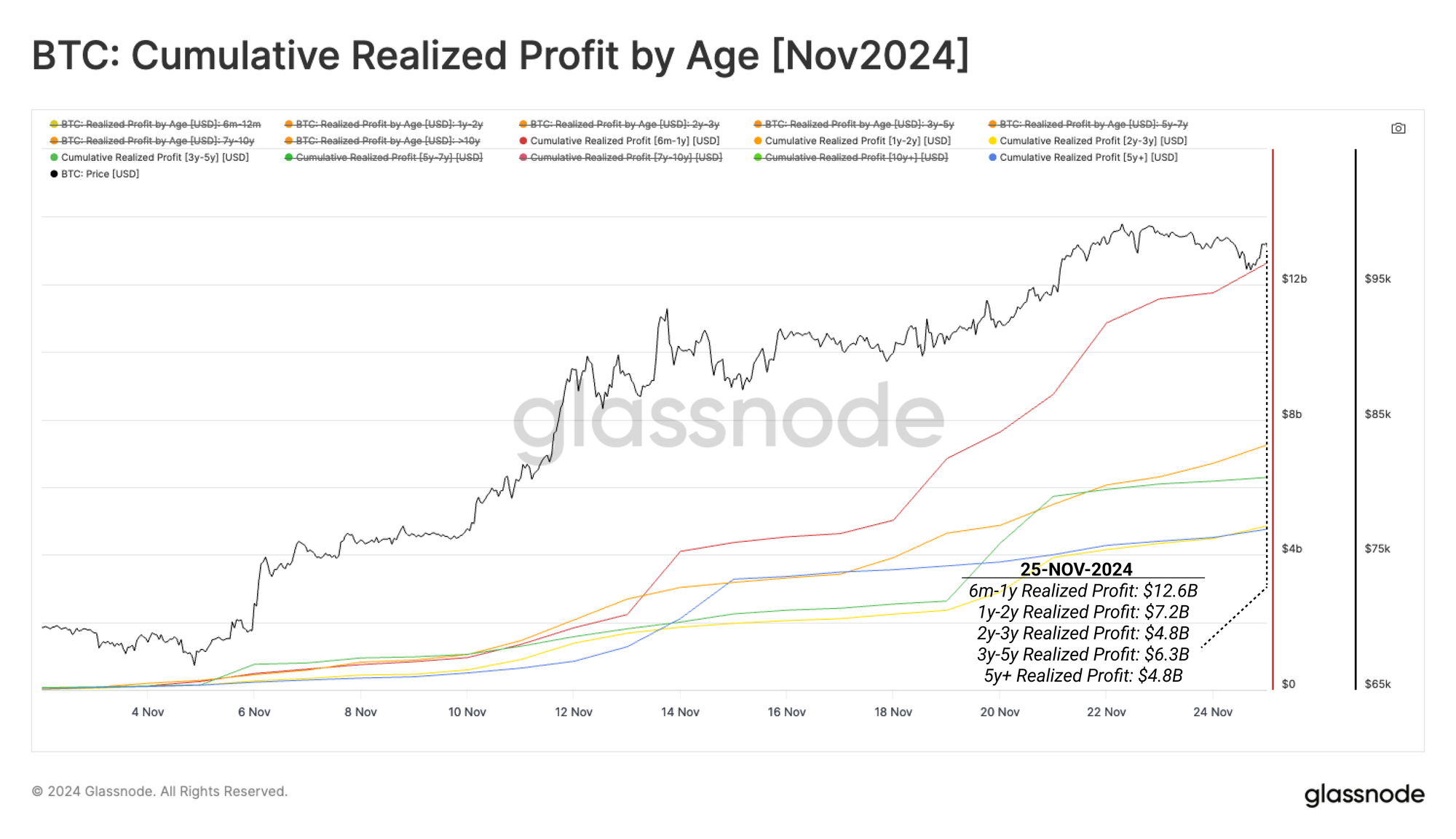

We can utilize our age breakdowns of the realized profit metric to evaluate which sub-cohorts are contributing the most to sell-side pressure. Here, we calculate the cumulative profit-taking volume by age since the start of the Nov-2024.

- 6m-1y Realized Profit: $12.6B

- 1y-2y Realized Profit: $7.2B

- 2y-3y Realized Profit: $4.8B

- 3y-5y Realized Profit: $6.3B

- 5y+ Realized Profit: $4.8B

Coins aged between 6 months and 1 year dominate the prevailing sell-side pressure, accounting for 35.3% of the total.

The dominance of coins aged 6m-1y highlights that the majority of spending has originated from coins acquired relatively recently, highlighting that more tenured investors are remaining measured and potentially waiting patiently for higher prices. One could argue that these selling volumes may describe swing trade style investors, who accumulated after the ETFs launch and planned to ride only the next market wave higher.

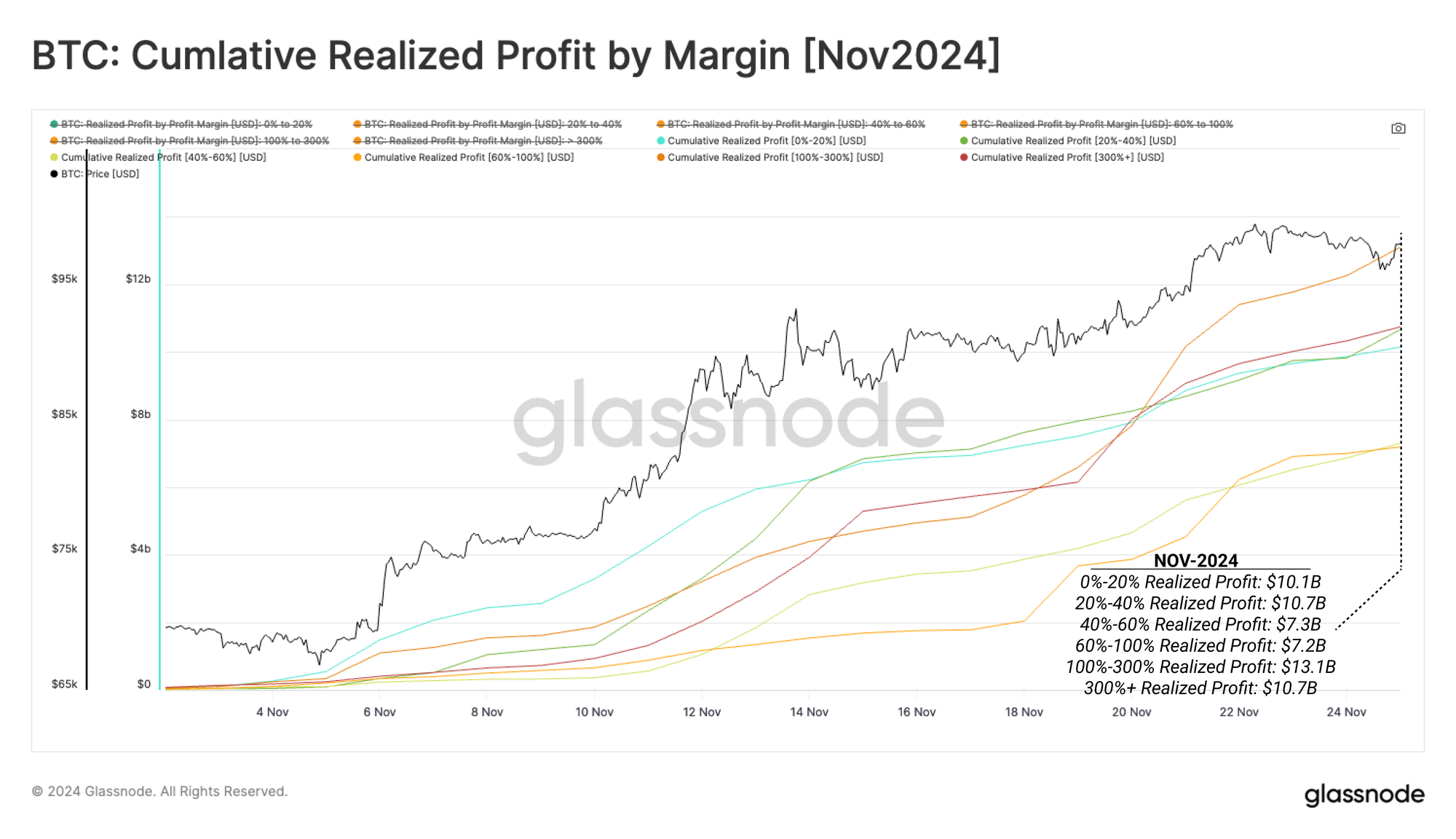

Following this, we can apply the same methodology to the magnitude of profit realized across all investors, segregated by percentage ROI locked in.

- 0%-20% Realized Profit: $10.1B

- 20%-40% Realized Profit: $10.7B

- 40%-60% Realized Profit: $7.3B

- 60%-100% Realized Profit: $7.2B

- 100%-300% Realized Profit: $13.1B

- 300%+ Realized Profit: $10.7B

Interestingly, these groups have a degree of uniformity, with all cohorts realizing a similar proportion of the total. It could be argued that this represents a ‘chips-off-the-table’ strategy, where investors with a lower cost basis achieve similar USD profit volumes by selling fewer coins over time.

Looking specifically at coins acquired during 2021, 2022, and 2023, we can observe both considerable and sustained spending behaviour in the March peak.

However, for the prevailing rally, spending predominantly consisted of coins acquired in 2023, with coins from 2021 and 2022 only starting to increase their sell-side pressure. This again aligns with a possible interpretation of ‘swing-trade’ style profit-taking as a dominant strategy.

Gauging Sustainability

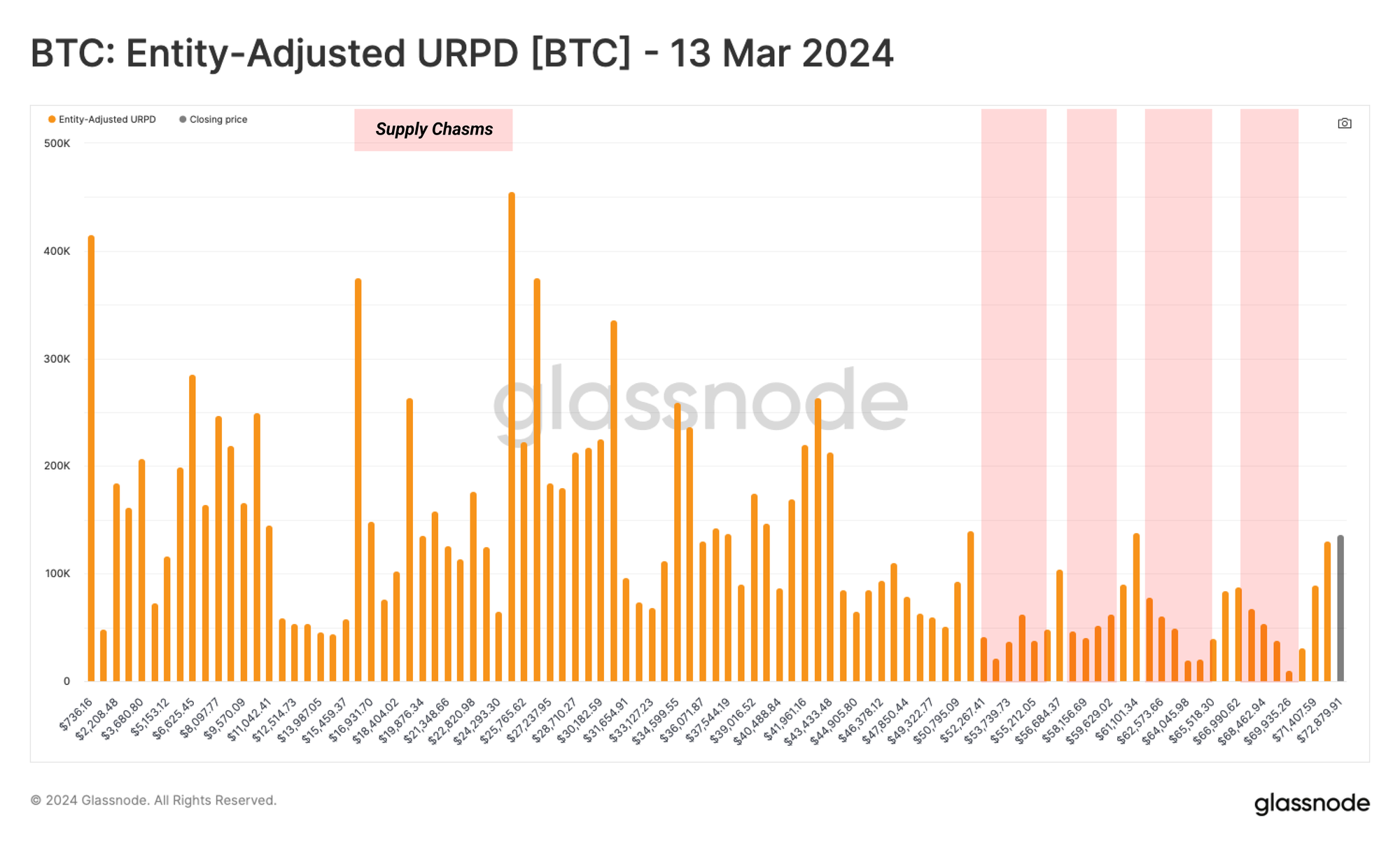

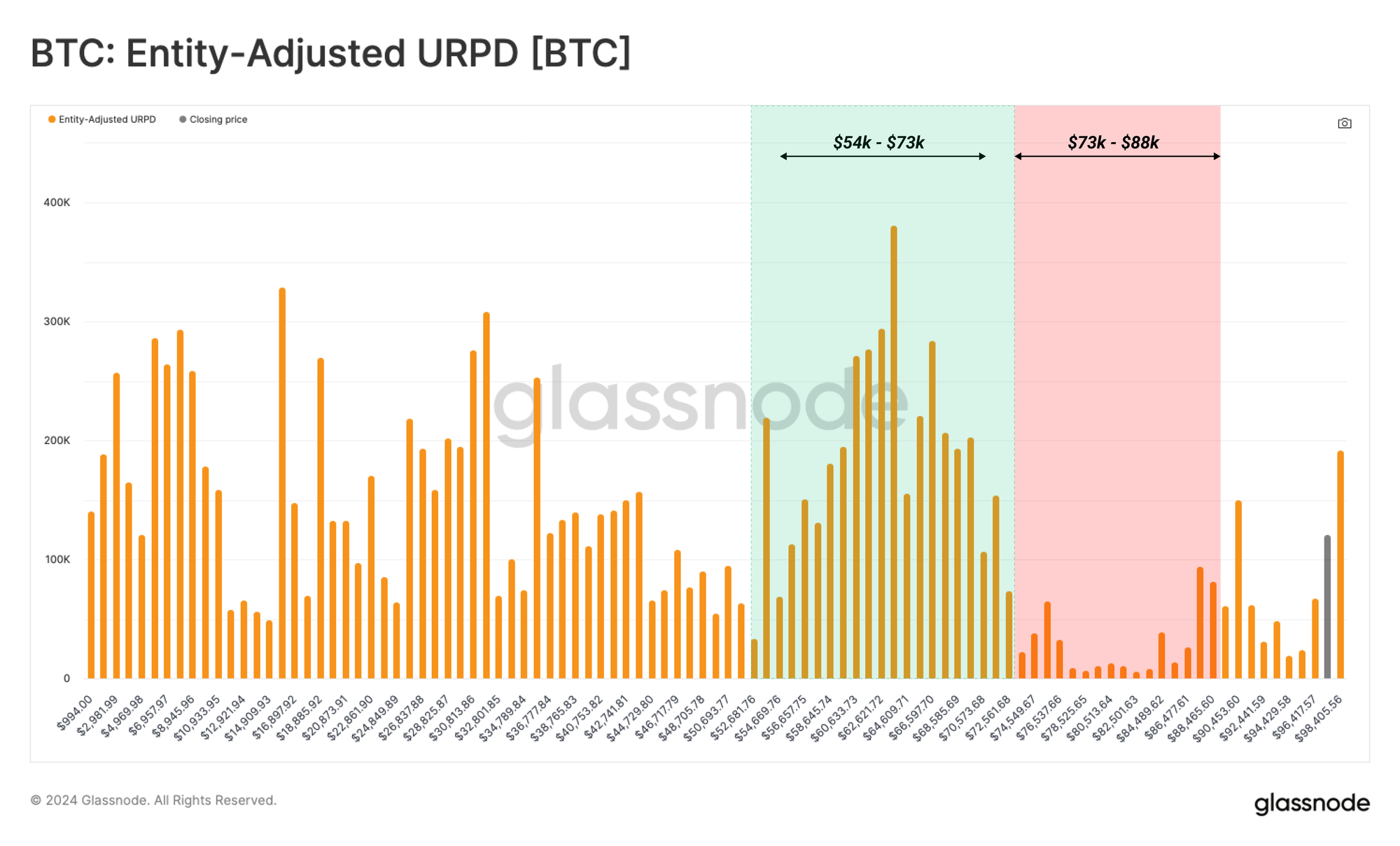

To gauge the sustainability of this uptrend, we can compare the structure of the current URPD to that experienced during the March 2024 ATH.

In March 2024, after several months of appreciation following the ETF launch, supply changed hands at several supply clusters between $40k and $73k ATH. Over the seven months of choppy price action that followed, this region became one of history's most significant supply clusters.

As supply was re-accumulated, it formed the eventual support from which this rally began.

Fast forwarding to today, the market rallied so quickly that very few coins changed hands between $76k and $88k. Two key observations can be ascertained from this:

- Price discovery is a process that tends to require rallies, corrections, and consolidations to confirm new price ranges.

- There is a sort of ‘air gap’ below $88k, which may become a zone of interest if the market corrects lower before re-attempting a move above $100k.

As the market attempts to re-find equilibrium in this price discovery regime, changes in the supply distribution can provide insight into supply and demand zones of interest.

Summary and Conclusions

Supported by surging price action, Long-Term Holders are meaningfully distributing coins, locking in a substantial $2.02B in profit. This has created an overhang of supply that must be absorbed to accommodate sustained increases in price.

When evaluating the composition of which entities are spending, the majority of this sell-side pressure appears to originate from coins aged between 6 months and 1 year. This underscores the potential for further distribution from older entities who require a higher price to part with their coins.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.

- Join our Telegram channel.

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio